02 : Projects

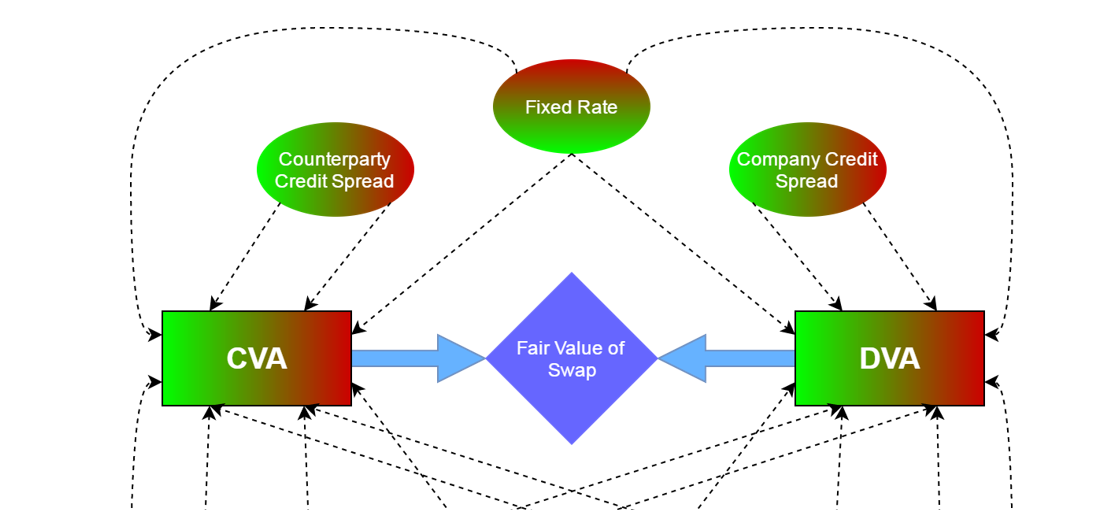

I am passionate about quantitative research and have developed projects that showcase my expertise in data science, financial modeling, and algorithmic trading. One of my notable projects is the "Value-at-Risk (VaR) Estimation Model for Multi-Asset Portfolio," where I implemented Monte Carlo simulations and historical simulations to compute VaR across diverse asset classes. This project enhanced my skills in risk management and financial analytics. Another significant achievement is the "Counterparty Credit Risk Model using CVA & DVA Adjustments," which involved pricing credit and debit valuation adjustments for OTC derivatives using Monte Carlo methods and hazard rate modeling. These projects highlight my proficiency in financial modeling, quantitative analysis, and Python programming.

001/005

Real-Time News Sentiment Signal Engine for Trading

Skills: NLP, Sentiment Analysis, Signal Engineering, Feature Engineering, Data Streaming Technologies: Python, FinBERT (HuggingFace), NewsAPI, Tweepy, pandas, NumPy, Streamlit

Discover

002/005

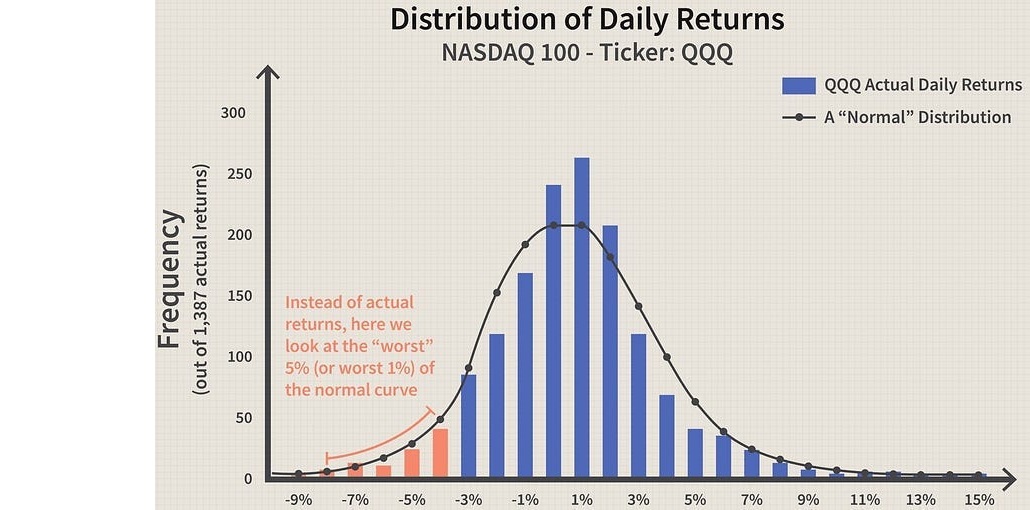

VaR-CVaR Estimation for AI Stocks and Bitcoin Correlated Portfolio

Skills: Risk Modeling, Monte Carlo Simulation, Copula Theory, Financial Engineering Technologies: Python, NumPy, pandas, SciPy, matplotlib, yfinance, copulas

Discover

003/005

Counterparty Credit Risk Model using CVA and DVA Adjustments

Skills: Credit Risk, CVA/DVA Modeling, Exposure Simulation, Survival Analysis Technologies: Python, NumPy, pandas, matplotlib, SciPy

Discover.jpg)

004/005

Value-at-Risk (VaR) Estimation Model for Multi-Asset Portfolio

Skills: Quantitative Risk Analysis, Portfolio Analytics, VaR Estimation Technologies: Python, pandas, NumPy, matplotlib, yfinance, SciPy

Discover

005/005

AI-Powered Intraday Market Making Strategy for Bitcoin Futures

Skills: Reinforcement Learning, Market Microstructure, Simulation, Deep Learning Technologies: Python, Stable-Baselines3, OpenAI Gym, NumPy, matplotlib

Discover