001 : Real-Time News Sentiment Signal Engine for Trading

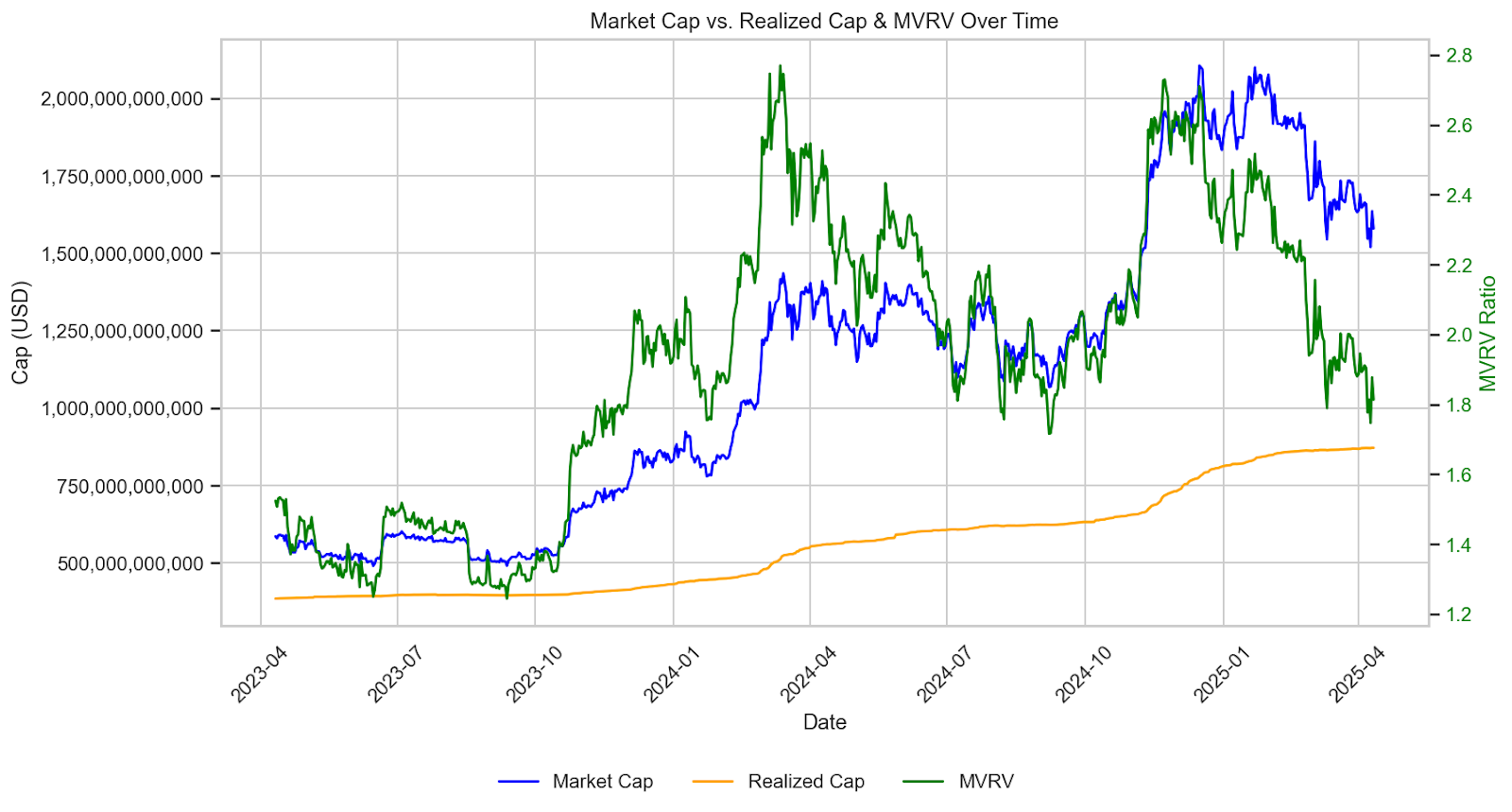

002 : VaR-CVaR Estimation for AI Stocks and Bitcoin Correlated Portfolio

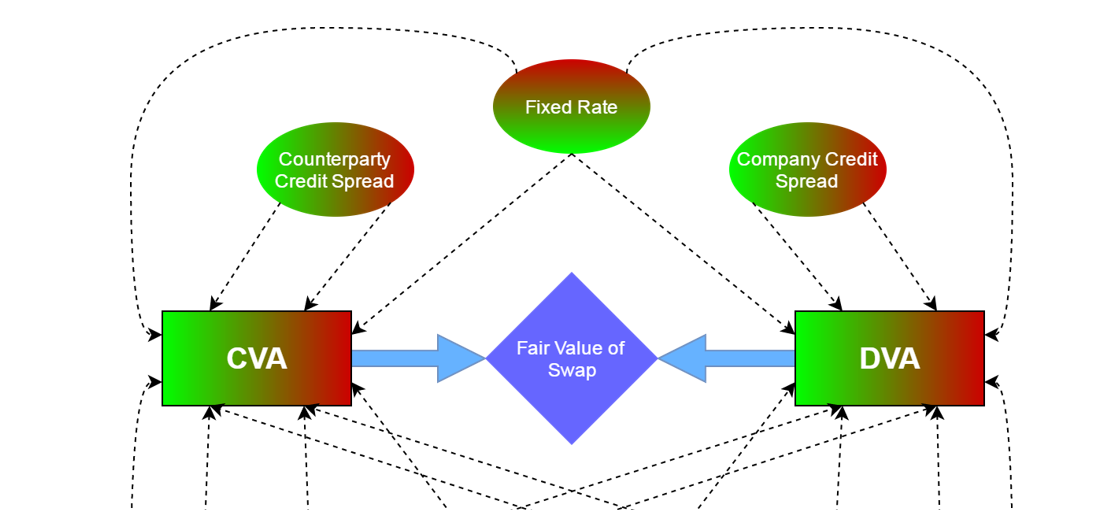

003 : Counterparty Credit Risk Model using CVA and DVA Adjustments

.jpg)

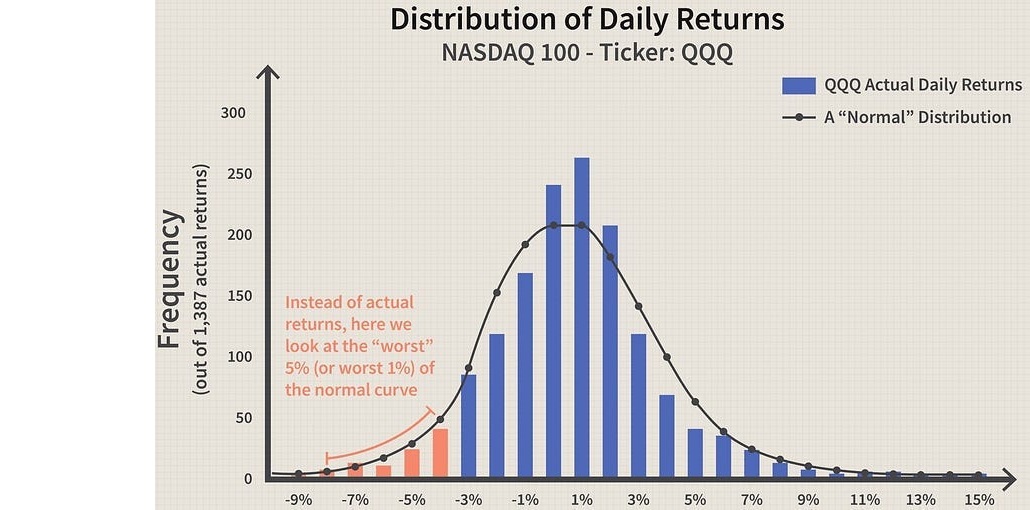

004 :Value-at-Risk (VaR) Estimation Model for Multi-Asset Portfolio